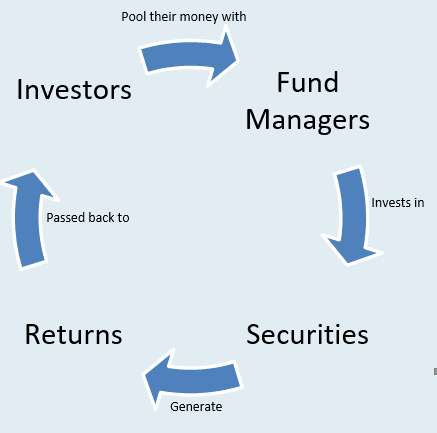

"A mutual fund is a collective investment scheme, which specializes in investing a pool of money collected from investors for the purpose of investing in securities such as stocks, bonds, money market instruments and similar assets."

One of the main advantages of mutual funds is that they give small investors access to professionally managed, diversified portfolios of equities, debt instruments i.e. TFCs and Govt. Securities and other securities, which otherwise would be quite difficult (if not impossible) to create with a small amount of capital. The income earned through these investments and the capital appreciations realized are shared with its unit holders in proportion to the number of units owned by them.

There are two types of Mutual Funds:

- Open-Ended Mutual Funds

- Closed-Ended Mutual Funds

These are mutual funds which continually create new units or redeem issued units on demand. They are also called Unit Trusts. The Unit holders buy the Units of the fund or may redeem them on a continuous basis at the prevailing Net Asset Value (NAV). These units can be purchased and redeemed through Management Company which announces offer and redemption prices daily.

Close-endedThese funds have a fixed number of shares like a public company which are floated through an IPO. Once issued, they can be bought and sold at the market rates in secondary market (Stock Exchange). The market rate is announced daily by the stock exchange.

Structure of Mutual fundsMutual Funds are operated by Asset Management Companies (AMCs) which exist in the form of public limited companies registered under Companies Ordinance, 1984. An AMC launches new funds through the establishment of a Trust Deed, entered between the Asset Management Company and the Trustee, with due approval from the SECP under the Non-Banking Finance Companies (Establishment and Regulation) Rules, 2003 (the “Rules”). The Trustee performs the functions of the custodian of the assets of the Fund. The Trustee ensures that the Fund Manager takes the investment decisions within the defined investment policy of the Mutual fund. Under Pakistan law, banks and central depository companies, approved by the SECP, can act as Trustee.

At present Central Depository Company of Pakistan (CDC) is acting as the Trustee for most of the funds of the industry.

The Securities & Exchange Commission of Pakistan (SECP) is the regulator of mutual funds industry and is very stringent in issuing licenses to fund management companies, especially in the case of Collective Investment Scheme (CIS). The SECP also carries out continuous monitoring of mutual funds through reports that the mutual funds have to file with the SECP on a regular basis. In addition, SECP conducts on-site inspections of the AMCs

Frequently Ask Questions

A fund's Net Asset Value (NAV) represents the price per unit. The NAV is equal to the market worth of assets held in the portfolio of a Fund, minus liabilities, divided by the number of units outstanding.

In order to determine the sale price of the unit, sales load is added to the NAV. In case there is no sales load, the NAV will be the sale price as well as the redemption price. The sale and redemption price is declared on a daily basis by the Funds and can be viewed on their websites.

Dividend PaymentDividend is paid in the form of cash on monthly/quarterly/annual basis depending upon the category of the fund and from AMC to AMC. Any investor who wishes to re-invest the dividend amount has the option to inform the AMC beforehand so the dividend amount will be re-invested and new units will be issued.

Taxation on Unit HoldersThe following information is provided for general informational purposes only. Since tax implications vary individually, investors are encouraged to consult their tax advisor to understand the specific tax consequences of investing in mutual funds

(1) Tax on Dividend U/S 150

As per section 150 of ITO, unit holders of mutual funds will be subject to Income Tax on Dividend Income received from a mutual fund as under:

| Tax Payer | Stock Funds | Other Funds* |

|---|---|---|

| Company | 15% | 25% |

| Individual/AOP | 15% | 25% |

A 25% tax rate applies if 50% or more of a Mutual Fund’s income is derived from profit on debt. This rate is considered final, and the Trustee is required to withhold the tax at source. The rate of tax will be doubled for investors not appearing on the Active Taxpayers List maintained by FBR. Unit Holders who are exempt from income tax can obtain an exemption certificate from the Commissioner of Income Tax. Upon presenting this certificate, income tax will not be withheld.

(2) Capital Gains Tax (CGT) (U/S 37A)

As per section 37A of ITO, AAML will deduct Capital Gains Tax at the rates as specified below, on redemption of securities:

| Tax Payer | Stock Funds | Other Funds* |

|---|---|---|

| Company | 15% | 25% (there is no change from last year i.e FY2024) |

| Individual/AOP | 15% | 15% |

No capital gains tax shall be deducted, if the holding period of the security acquired on or before 30th June 2024 is more than six years.

Risk DisclaimerAll investments in mutual funds are subject to market risks. The NAV of units may go up or down based on market conditions. Past performance is not necessarily indicative of the future results. The investors are advised, in their own interests, to carefully read the Offering Document, in particular the investment policies and risk disclosure and warning statements in their respective Offering Document.

SECP, the Regulator, has categorized the Schemes of mutual funds as under:-

Equity Scheme:An equity scheme or equity fund is a fund that invests in Equities more commonly known as stocks. The objective of an equity fund is long-term growth through capital appreciation, although dividends and capital gain realized are also sources of revenue.

Balanced Scheme:These funds provide investors with a single mutual fund that invests in both stocks and debt instruments. This diversification is aimed at providing investors a balance of both growth through investment in stocks as well as income from investments in debt instruments.

Asset Allocation Fund:These funds may invest their assets in any type of securities at any time in order to diversify their assets across multiple types of securities & investment styles available in the market.

Fund of Fund Scheme:Fund of Funds are those funds, which invest in other mutual funds. These funds operate a diverse portfolio of equity, balanced, fixed income and money market funds (both open and closed ended).

Shariah Compliant (Islamic) Scheme:Islamic funds are those funds which invest in Shariah Compliant securities i.e. shares, Sukuk, Ijara sukuks etc. as may be approved by the Shariah Advisor of such funds. These funds can be offered under the same categories as those of conventional funds.

Capital Protected Scheme:In this type of scheme, the payment of original investment is guaranteed with any further capital gain which may accrue at the end of the contractual term of the Fund. Such funds are for a specific period.

Index Tracker Scheme:Index funds invest in securities to mirror a market index, such as the KSE 100. An index fund buys and sells securities in a manner that mirrors the composition of the selected index. The fund's performance tracks the underlying index's performance.

Money Market Scheme:Money Market Funds are among the safest and most stable of all the different types of mutual funds. These funds invest in short term debt instruments such as Treasury bills and bank deposits.

Income Scheme:These funds focus on providing investors with a steady stream of fixed income. They invest in short term and long term debt instruments like TFCs, government securities like T-bills/ PIBs, or preference shares.

Aggressive Fixed Income Scheme:The aim of aggressive income fund is to generate a high return by investing in fixed income securities while taking exposure in medium to lower quality of assets also.

Commodity Scheme:These schemes enable small investors to take advantage of gains in commodities, such as gold, through pooled investments. They invest at least 70% of their assets in commodity futures contracts, which include both cash-settled and deliverable contracts.

An investor can invest in any of the above categories of funds in accordance with his requirements and appetite for risk. For example, those who want to earn high returns over a longer period can invest in Equity Funds, whereas those who want to invest for short term with reasonable return can invest in Money Market Fund.

Investing directly in stocks is relatively riskier than investing through Mutual Funds From where do you get the vegetables for dinner? Do you grow them in your backyard, or purchase them from the nearest mandi/supermarket depending on what you need? Growing your own veggies is a great way of eating healthy food, but effort is spent on seed selection, manuring, watering, pest control, etc. The latter option allows you to choose from a wide variety without the hard work.

Similarly, you can create wealth by either investing directly in shares of good companies or investing in them through Mutual Funds. Though wealth can be created when we buy company stocks which use our money to grow their business, direct investment in shares carries a relatively higher risk element. You need to pick stocks by researching the company and sector. It;s a humongous task to choose a few companies from hundreds of them listed on the stock exchange. Once invested, you need to keep a track of every stock's performance for purchase and sell transactions.

In Mutual Funds, all the market research and stock picking is done by expert fund managers. All you need to do to keep track is to follow the performance of the fund rather than following individual stocks within the fund. Unlike stocks, Mutual funds also allow investment flexibility with growth/dividend options, top-ups, systematic withdrawals/transfer, etc. besides helping to ride over market volatility by investing smaller amounts regularly through Systematic Investment Plans.

As conventional investors, we have the inclination to save more and secure our investments to the maximum extent possible. No one wants to risk his hard-earned money, so the security of an investment product is the first thing we analyze while investing. We are fortunate as compared to our previous generations who sought to invest at a time when the capital market was not as developed and the investment products available were not as regulated as they are today.

With the development in the products and their security features, we have the advantage of making wise investments through conscious and well-informed decisions. People are now willing to take more risk to get quicker returns, their disposable income has increased, markets are more developed and far more choices of investment products are available which have not only encouraged investors to invest but also promoted the savings and investment concept as an established norm. One of the most popular product as per investors choice is Mutual funds.

There are different connotations of the concept of “safe investments” as per different investors. For some, safe means guaranteed returns, for others it may mean principal preservation while for some, it may mean aggressive growth irrespective of market conditions.

A safe investment doesn't only depend of the product you choose, rather it also depends on your understanding from the time you pick your product which includes understanding your own risk profile, time horizon, financial needs and purpose of investment.

The most secure product considered by our elders was Fixed or recurring deposits, because they are managed by the banks which are regulated entities. The logic was simple: banks are supposed to have a huge deposits with them so could almost guarantee return on investments.

With the development of investment products, we have attractive choices among Mutual funds, some of which can give more attractive returns than conventional deposits. The value proposition of Mutual funds is the minimization of risk, even though the returns may not be guaranteed. Since Mutual funds are managed by professionals and experts, anyone with minimal investment knowledge can also invest in such funds. The risk is also reduced with diversification, as Mutual funds invest in a portfolio which is a combination of securities, rather than betting on single stock or bond, so the risk is divided among various securities. You can timely review the performance of your Mutual fund so as to switch you investments as and when needed.

You must have heard or read about Mutual funds being subject to market risks, so please read all scheme related documents before investing. This holds true not only for Mutual funds, but also for any product that you may want to invest in. It is really important that you understand the product's risk, where it invests, and the performance of the Asset Management

When it comes to safety of investment, investors are mostly concerned about 2 things

- Capital protection

- Fraud protection

This can be ensured by choosing investment which suits you, so as to save you from unnecessary losses. Conservative investors should focus on hybrid funds or debt funds and avoid investing in small and mid-cap funds where volatility is quite high.

Fraud protection:It;s a no less than a nightmare if someone runs away with your hard-earned money. This may make you wonder how safe it is to invest in Mutual funds. To safeguard investor interests, Mutual funds are regulated by the Securities and Exchange Commission of Pakistan (SECP). All Asset Management Companies (AMCs) and Investment Advisories (IAs) are licensed by SECP to launch Mutual Funds and perform Investment Advisory Services. AMCs are required to follow due diligence before taking investor;s money. AMCs cannot simply shut down and get away with your money which makes Mutual fund just as safe as banks.

Many investors are also skeptical about investing via distributors. Kindly be rest assured that even if tomorrow the distributor;s or agent;s company is closed, you can always reach the AMC of the Mutual fund and redeem your units.

Different types of risk associated to mutual funds:- Market risk

- Liquidity risk

- Credit risk

- Interest rate risk

The Securities and Exchange Commission of Pakistan in exercise of the powers conferred under section 2828(3) of the Companies Ordinance, 1984 read with regulation 66A(d) of the Non-Banking Finance Companies and Notified Entities Regulations, 2008 hereby prescribes the following requirements for AMCs to classify Collective Investment Schemes (CIS) and investment plans as per the following risk profiles:

| Category of CIS Plans | Risk profile | Risk of principal erosion |

|---|---|---|

| Money Market funds - AA and above rated banks and money market instruments | Very low | Principal at very low risk |

| Capital Protected Funds (non-equity), Income funds with investment in A or above rated banks, money market instruments (AA category and above) and investment in up to 6 months floating rate Govt. securities or Govt. backed sukuks, MTS. | Low | Principal at low risk |

| CPPI Strategy based fuds, Income funds (where investment is made in fixed rate instruments or below A rated banks or corporate sukuks or bonds, spread transactions, Asset Allocation and Balanced Funds with equity exposure up to 50% mandate). | Medium | Principal at medium risk |

| Equity Funds, Asset Allocation (with O - 100% Equity exposure mandate) and Balanced Funds (with 30 - 70% Equity exposure mandate), Commodity Funds, Index Trakker Funds and Sector Specific Equity related Funds. | High | Principal at high risk |

Mutual funds make saving and investing simple, accessible, and affordable. The advantages of mutual fund include the following:-

-

Accessibility

Mutual funds units are easy to buy.

-

Liquidity

Mutual fund unit holders can convert their units into cash on any working day. They will promptly receive the current value of their investment. Investors do not have to find a buyer; the fund buys back (redeems) the units.

-

Diversification

By investing the pool of unit holders; money across number of securities, a mutual fund diversifies its holdings. A diversified portfolio reduces the investors; risk. It would be difficult for an average investor to buy varied securities to achieve the same level of diversification as is available with investment in mutual fund.

-

Professional Management

Asset Management Company evaluates all the opportunities that arises in the market, carefully examines them and then takes decision for investing the mutual fund;s money whereas it is not an easy task for an individual and even for corporate company if investing is not their core business.

There;s a common misconception that Mutual Funds are not a Halal investment avenue. Well, this is certainly not true. Contrary to popular belief, most Mutual Funds in Pakistan have divisions which are regulated under Islamic Shariah Compliant policies.

1. All Islamic Investments are regulated by Islamic ExpertsSo who ensures that the investment is Halal? The most important aspect of Islamic Mutual Investments is that they are managed and supervised by renowned Islamic experts. These experts take extreme care to ensure that all aspects of the investment transactions are executed as prescribed by Shariah. This means that the investor does not have to worry about his investment not being Halal.

2. Capital is invested in Halal Equities and SecuritiesThe investor;s capital in an Islamic Mutual Fund is invested in companies and organizations which are run under Shariah compliant policies. This rules out any concerns an investor might have related to his capital being used for unethical means.

3. Islamic Investments are Interest FreeWhenever banking is involved, one of the first concerns of any customer is interest. Being prohibited strictly by Shariah, interest is a major concern for most people. Islamic Investment Funds make returns on capital in a way that the provider is willing to share in the risks of a productive enterprise. This means that capital in a way is lent and not invested, leading to interest being the return and not the profit. This means that the investment is devoid of interest.

4. Strict Criteria for Choosing Equities is FollowedIn order for an equity to be Shariah Compliant, it is necessary that the core business of the company should not violate any principle of Shariah. It is prohibited to acquire shares of companies which provide services on interest such as conventional banks, insurance companies, leasing companies. In addition to this, companies involved in certain other businesses are not approved by the Shariah, for e.g. companies making or selling liquor, pork, haram meat, or involved in gambling, etc.

Islamic Investment Funds are the perfect option for someone who wishes to save and invest to meet their short and long term financial goals. Whether it be saving for your child;s future or to go on a family vacation, with Islamic Investment Funds, you can easily do so by remaining within Shariah regulated boundaries.

How to choose mutual funds for investment? Ways to analyze mutual funds 1. PerformanceAn important aspect you should look at is the 'Performance Ranking' of a fund among its peers.

Rather than looking at a fund;s performance in isolation, it should be compared with similar funds on a monthly, quarterly, and annual basis. A fund that is consistently in the top quartile or decile should be preferred over others.

The past performance of funds managed by an AMC is a good indicator to see if your savings are in good hands.

2. Ratio analysisA 'Ratio Analysis' of the fund helps in analyzing its risk and return. Ratios such as standard deviation, sharp ratio, and measurement of Alpha helps in comparing your fund of choice with the other funds on offer.

The Alpha of a fund should be of particular interest, as it will tell you how much a fund manager has been able to outperform or underperformed a benchmark. The Alpha of any given fund, along with the other ratios, is available in the monthly Fund Manager Report (FMR) published by the AMC.

The 'Total Expense Ratio' tells you about the total fund management and distribution related expenses. A higher expense ratio will adversely affect the fund;s returns and is generally not desirable.

3. Tenure and experienceThe tenure of your fund's manager (AMC) and its experience and expertise are also important things to look at when selecting a fund. The fund manager is the final decision maker regarding any investment decision related to the funds. Its expertise and investing style will greatly impact the performance of a fund, and you should always try to find more out about the manager of the fund.

4. Size of the fundThe size of a mutual fund is another important factor in the selection of a fund. Funds with small Assets Under Management (AUM) are exposed to concentration risk. When a large investor exits or redeems their investment from a fund with a small AUM, the fund may be impacted adversely and the remaining small investors may have to suffer.

When an average salaried person decides to save, the first thing they need to keep in mind is the fact that a 100 rupees saved today sadly will not have the same purchasing power tomorrow. This is due to the economic phenomenon known as 'inflation'.

You will have experienced inflation from the changes in prices of the daily goods we buy, the tuition fee we pay for our children, and the medical bills we pay for ourselves and our loved ones. What was worth Rs. 50 a year ago, may today be worth Rs. 100.

This means that simply saving money will do you more harm than good.

To counter the impact of inflation, your savings will need to grow at a rate that is either equal to or higher than the general increase in prices in the economy.

Should I Invest in mutual funds?We may understand the benefits of investing in a mutual fund as compared to investing on our own by looking at this simple example:

Consider driving yourself every day to work and coming back in your own private car. Commuting in your own car gives you the flexibility to decide when to travel, what stops to make and what route to take. However, on the downside you would have to constantly think about taking the shortest and best route, wrestle through the traffic, endure stress, pay the extra amount for fuel consumption, and forego the work you could do if you were not driving.

On the other hand, if you were to travel in a public bus, you would just have to buy a ticket and board the bus. Once you are in the bus, the experienced driver, in our case the fund manager, would do all the hard work for you, and while commuting on the bus you could work on other tasks and save on the extra costs when travelling solo in your own car.A mutual fund offers the same ease as the public bus has over the private car. You may invest and see your investments grow over the years.

It is a collective investment scheme in that a lot of people contribute their savings to a central fund. A professional and experienced fund manager can assess the situation and invest your money in a variety of investment options.

- Risk Factor

- Asset Allocation

Having a built up portfolio of assets is all well and good, but managing a large portfolio is easier said than done, and often takes up significant chunks of time.

Asset managers and asset management companies help their clients manage their portfolios and make investment decisions based on extensive research. Here are some of the factors to consider when choosing an asset manager:

Research the CompanyWith any asset manager, the first thing you should check is their credentials. This will determine whether they are legitimate, and give you an insight into their experience and what they can do for your investment portfolio.

Asset management firms usually have numerous advisers who may specialize in different fields of investment, so it is worth seeing what the firm;s capabilities are and how they may cater to your specific requirements as an investor. It is also important to know exactly how they operate and go about investing your capital.

History/RegulationAnother consideration is how well established the asset manager is, and what their history of asset management looks like. Looking at their past successes (or failures) is a good way of determining whether they will work for you. If they are currently managing assets for thousands of clients and have good testimonials on their site, then the chances are they are an effective and trustworthy firm.

PriceObviously, the most important factor for many investors when choosing an asset manager is the cost of the service. This can vary greatly between companies, and depends on which services you intend to use.

It is often the case that larger asset management companies, which manage billions or even trillions of worth of assets, can offer cheaper prices whilst still remaining very profitable. That being said, there are still smaller firms which may be just as effective in meeting your requirements, if not more so. You may also get more personal, in depth experience with a smaller firm. Comparing the price of different wealth managers and listing them will go a long way in helping you determine which one to choose.

Whenever choosing an asset manager, be very thorough in your research, and do not hesitate to contact them to find out further details about their service. Once you have managed to decide which one you would like to manage your assets/investments, you should review them regularly and make sure they are fulfilling your long term investment goals.

Picking the right fundYour plan must be based on investment objectives and risk appetite.

For example, if you want to save for a car (or place your savings in a fund that is easily accessible at any given point in time), then you should invest in a cash fund.

However, if you are looking to invest for your child;s college education or are looking for long-term savings, a balanced fund (where investments are balanced between stocks and other assets e.g. bonds), or an equity fund (stock market focused).

Capital preservation funds on the other hand provide the best of both these worlds. They allow you to access your investment when required.

Emlaak offers the simplest and easiest experience for investing in mutual funds. The portal has been designed in line with its vision to facilitate investors in making informed decisions. It offers a convenient, informative and interactive medium to invest in a wide range of investment products offered by different fund families.

By creating an account through Emlaak Financials, you, as an investor, can avail the following benefits:

- Simplified online account opening: Simply select the fund of your choice, click to invest, fill in your particulars (CNIC, address, nominee) and amount to invest and proceed to payment.

- Hassle-free online investment, redemption and conversion transactions

- Consolidated dashboard of investments

- Online account statement generation

- Comprehensive information and helpful analytics of all mutual funds

You can completely make your own investments, using the industry data analytics presented on the portal which help you in making informed decisions.